ABA May/June 2026: Two Sides of the Same Coin

BANKS KNOW THAT COMPLYING with the complex and ever-changing body of federal and state regulations is a cost of doing business. Savvy institutions also recognize that well-designed compliance toolkits can advance business objectives as well as support revenue growth.

While the Department of Justice (DOJ) and prudential bank regulators require banks to maintain programs to ensure compliance with fair lending laws and the Community Reinvestment Act (CRA), strong fair lending and community reinvestment compliance practices can also help identify strategic business opportunities for growth. With slight modifications to existing approaches, analyses conducted as part of existing fair lending and CRA compliance programs can also highlight areas of competitive strength and weakness in a bank’s current and potential target markets.

By repurposing compliance tools for business-line consumption, low-hanging competitive opportunities, gaps in product sets or services, and potential growth partnerships may come into focus.

This article offers practical suggestions for applying a fresh lens to fair lending and CRA compliance tools, such as peer analysis, mapping, and performance context, across a variety of situations. It helps banks identify actionable strategies for growth and maximize the impact of compliance teams on the bank’s bottom line, while maintaining strong CRA and fair lending programs.

Market intelligence as a growth tool

Fair lending and CRA compliance teams conduct a wide variety of quantitative and qualitative analyses to identify risks and support action plans to manage them appropriately, but these analyses can serve dual functions. Banks can leverage the same market-based information used for fair lending and CRA compliance to identify targeted areas of competitive opportunity.

Market-penetration or "peer" analyses, mapping, and performance context are three types of reviews commonly conducted by banks of all sizes. By using these analyses to answer growth questions, banks can implement high-impact actions to gain or reinforce a competitive edge.

Peer analyses: Useful for identifying gaps and strengths

Bank fair lending and CRA programs typically conduct or oversee statistical analyses to evaluate the bank’s performance in receiving applications and originating loans in all segments of the bank’s markets, including comparisons to competitors in the same markets. The analyses typically track requirements and expectations that regulators have historically communicated through rules, guidance, and public enforcement actions.

For example, regulators and enforcement agencies expect banks to monitor redlining risk through statistical peer analyses that evaluate the bank’s performance in majority-minority census tracts (including majority-Black, Hispanic, or in other demographically-defined areas) and non-majority-minority tracts within its service areas as compared to that of peer lenders. Banks evaluating their CRA performance assess how well they meet the credit needs of all segments of their communities, including low- and moderate-income (LMI) communities and borrowers, by analyzing their lending patterns in LMI census tracts and with LMI borrowers relative to their peers.

From fair lending and CRA compliance perspectives, these analyses indicate whether application and origination activity differs from peer institutions in statistically and materially different ways.

If the bank identifies statistically significant differences in its penetration of defined census tract segments, the analyses may provide additional contextual information to help evaluate the performance gaps. For example, they may show the shortfall in applications or loans needed to close the gap, or more granular information regarding the loans made by peer lenders.

The same peer analyses conducted to monitor CRA and fair lending risk contain valuable market intelligence that can answer strategic growth questions. Peer analyses most typically evaluate a bank’s performance in CRA assessment areas, metropolitan statistical areas (MSAs), or metropolitan divisions (MDs) within an MSA. Still, banks can use the underlying data to zero in on smaller geographies with high growth potential. Peer analyses can provide even more granular information about any observed lending penetration gaps, such as a list of census tracts where other lenders have generated material application volume.

However, if a bank has received few, if any, applications in certain census tracts, or receives applications that do not result in funded loans while peer institutions are originating loans in those areas — this may indicate a competitive gap or elevated redlining risk. Analyzing the tract lists where the bank is underperforming can support strategies for microtargeting to increase name recognition, rebalancing loan officer coverage, monitoring leads, and more.

Compliance reporting appropriately focuses on areas presenting the greatest fair lending and CRA risks, but by carefully analyzing success stories, business lines can use the data to spur growth in new ways. Peer analyses showing statistically significant favorable results demonstrate the bank’s existing dominance in a particular market relative to other lenders, and the bank can use this information to expand its competitive advantages further.

Banks should evaluate the factors driving high-performance observations and consider whether they can replicate successful approaches in other areas. Exploring the strategies that underpin success stories can position banks to advance growth in underperforming or stagnant markets.

Mapping: Visualizing market opportunities

Banks regularly conduct mapping analyses that visually display residential mortgage, small business, or small farm applications and loans across the geographic area they serve. These maps support a range of fair lending and CRA compliance objectives. For example, banks compare applications and originations inside and outside their delineated CRA assessment areas to monitor geographic lending patterns relative to areas with concentrations of minority or LMI populations. Mapping also helps banks evaluate potential adjustments to assessment area delineations. Additionally, banks map branch and other physical locations to assess market coverage, travel-times, and geographic deposit concentration.

As with statistical peer analyses, mapping can serve as a dual-purpose tool for identifying areas to target for growth and investment. By mapping lending activity or physical locations on shaded maps that also depict CRA assessment area boundaries, MSA/MD boundaries, county lines, major cities, and major highways, business unit leaders can more easily identify areas where the bank has a dominant presence and where unexplained gaps may exist.

To meet CRA requirements, compliance programs appropriately focus on LMI geographies and borrowers, but mapping analyses can also help identify credit-access gaps in middle- or upper-income areas, including areas with concentrations of minority populations. Mapping analyses can also help identify LMI and non-LMI tracts that appear to be banking deserts. This can help a bank to meet customer needs better by deploying micro-branches, loan production offices (LPOs), shared space, or mobile bankers.

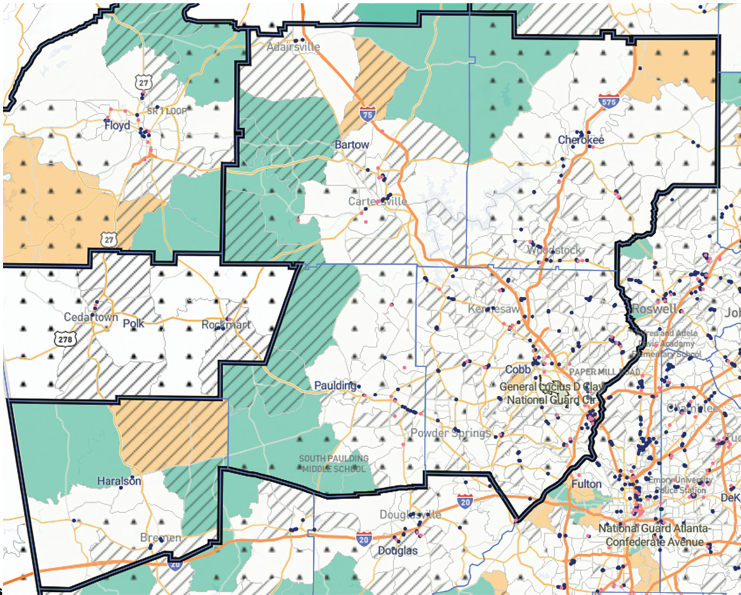

Figure 1: Identifying expansion opportunities in high-growth census tracts

By incorporating deposit accountholder addresses and branch and LPO locations with HMDA, CRA small business/small farm, or other lending data, a bank can create a robust picture of its market penetration across tract types. Publicly available Summary of Deposits data lets you consider competitors’ locations as well as your own.

Are there areas within a bank’s markets where it lacks a physical presence while peers operate branches? If peer lending activity is strong but the bank has little or no lending or deposit activity in those areas, the market may be ripe for additional outreach, LPOs, or branch network expansion. Conversely, if the bank has a physical presence but limited deposit or loan customers, this is a signal to reassess marketing and engagement strategies in these areas. However, if your customer base is substantial in areas without physical locations, it may indicate effective use of digital channels.

Mapping can also be a useful tool in identifying potential new locations. The map shown of a metro Atlanta suburb in Figure 11 overlays census tracts with no branches (green areas) or only one branch (orange areas) with highest owner-occupied housing quartiles. A review of census data reveals these areas also have significant population growth.

For example, let’s consider the Marietta Metro Division. Cherokee County grew by more than 30% between the 2010 and 2020 census enumerations, and the county expects an additional 50% increase in population by 2050. Paulding County’s population grew by nearly 40% between 2010 and 2020. Despite the substantial growth, there is a dearth of bank and credit union branches in middle- or upper-income census tracts with high levels of owner-occupied housing and substantial growth. These high population, low branch areas might be opportunities for strategic expansion.

Performance context: Understanding local market conditions

Because socioeconomic conditions and community credit needs vary considerably by market, the performance context analysis is a core part of bank CRA evaluations. To ensure uniform application of CRA requirements across banks operating in diverse markets, CRA examiners conduct performance context analyses and develop research-based descriptions of market conditions within banks’ assessment areas.

According to regulatory guidance, "the performance context is a broad range of economic, demographic, and institution- and community-specific information that an examiner reviews to understand the context in which an institution’s record of performance should be evaluated."2 Compliance teams conducting CRA performance reviews also complete performance context analyses by considering:

Demographic data on income level and distribution, housing stock, housing costs, and unemployment;

Data on lending, investment, and service opportunities in the bank’s assessment areas obtained from the bank itself or from community organizations, state or local government authorities, economic development agencies, or other sources;

Data on levels of banking and lending competition in the market; and the

General economic climate at national, regional, and local levels; and more.

Consistent with regulators’ practices, many bank compliance teams meet with community contacts in their assessment areas to discuss local market conditions and credit needs.

A carefully conducted performance context analysis can impact a bank in ways that extend far beyond developing a framework for fairly assessing CRA performance. Business lines can leverage the same data and information underlying the performance context analysis to improve their understanding of local market trends, the nuances of differing credit and banking needs across community segments, and barriers to credit access. Then they can use that knowledge to create unique business opportunities.

Case study: Addressing an unmet community credit need

In one case, a bank conducting a community credit needs assessment met with a city housing authority and learned of the city’s struggles to disburse grant funds earmarked for home winterization. The program required a roof inspection as a condition of approval, and the city observed that it frequently denied winterization grant applications because the homes did not pass the roof inspections and the applicants lacked the funds to pay for necessary roof repairs. The bank developed a small-dollar home improvement loan program to meet the credit need. It was the only loan program of its kind offered in the area and was successful in generating loan originations.

Using expanded data to strengthen performance context

Mapping and statistical analysis of expanded lending data can also help build performance context, particularly in areas where the bank has lower levels of HMDA- or CRA-reportable lending activity. For example, overlaying auto or other consumer loans on lending maps can help demonstrate that the bank is serving its communities with needed credit products, even in areas with lower levels of HMDA- and CRA-reportable lending. This is particularly true if consumer lending is an important part of your institution’s credit portfolio, or if the bank serves areas with limited need for mortgage loans.

For example, in rural areas, auto loans are an important consumer credit need. The absence of public transit and limited service by taxi or rideshare companies, combined with greater distances to employment centers, makes a car a requirement for both employment and educational access.

Another long-term growth question that a performance context analysis can help answer is: Has the bank developed and maintained a network of community partnerships and referral sources that sufficiently reaches all market segments? Thinking beyond core CRA relationships with Community Development Financial Institutions, community development corporations, and HUD-approved housing counselors: Has the bank engaged municipal housing and community development departments or divisions? Small business incubators? Local chambers of commerce?

By identifying each market’s trusted advisors and pursuing non-traditional partnerships, banks can reach more broadly than their competitors and lay the groundwork to foster growth.

Product and service offerings and design

Fair lending and CRA compliance teams regularly evaluate product and service offerings. From a fair lending perspective, the bank reviews products and services as part of fair lending risk assessments to meet regulatory expectations for identifying, monitoring, and managing risk. Federal regulators responsible for examining compliance with fair lending laws have observed that an "institution that offers a variety of lending products or product features … may benefit consumers by offering greater choices and meeting the diverse needs of applicants." Also, examiners assess whether the bank offers "programs that are specifically designed to assist certain borrowers," such as "conventional ‘affordable’ housing loan programs."3

Under the prior administration, redlining complaints filed by the DOJ reveal the fair lending risks that may arise from product suites that lack options to address the needs of the full range of customer segments within a lending market. DOJ consent orders related to redlining require banks to conduct and analyze the steps taken to revise mortgage lending policies and practices that pose redlining risks, including a review of the types of loan products offered by the bank. The consent orders also require banks to conduct a research-based market study, referred to as a "community credit needs assessment," to help identify financial services needs in the allegedly redlined area, including an analysis of loan products offered by other lenders operating in the same geography.

CRA compliance teams also review the bank’s products and services. "Responsiveness" to credit and community development needs is either a criterion or otherwise a consideration in the CRA performance tests. Information regarding the products and services offered by a bank can evidence the bank’s responsiveness in CRA examinations where examiners "evaluat[e] the range of services provided in geographies of different incomes."4

By repurposing compliance tools for business-line consumption, low-hanging competitive opportunities, gaps in product sets, and potential growth partnerships may come into focus.

While not establishing a formal list of information that demonstrates the responsiveness of a bank’s products and services, CRA guidance noted "practical suggestions of the types of information institutions could collect or maintain to demonstrate the responsiveness of a community development service," including "surveys completed by the financial institution to ascertain community needs," "an institution’s records of discussions with community contacts," and "publicly available market research data that support the importance to low- or moderate-income families for a particular type of service."5

This fair lending and CRA guidance underscores the importance of reviewing product and service offerings to help mitigate fair lending risk and advance CRA performance examination goals. However, a bank can also use the same analyses to identify business opportunities for expanding product and service offerings to compete better with peers in its markets.

If peer analyses reveal gaps in a bank’s lending performance by borrower income level or to neighborhoods by tract level income compared with other lenders, the bank should compare its product suite with those offered by competing lenders. The analyses may reveal that peer lenders who are the most successful offer certain products or product features that are missing from the bank’s offerings.

Leveraging community relationships and outreach

Banks commonly collect feedback from attendees or community partners during financial education and other community outreach events they host or sponsor. Ongoing conversations with community partners can help identify emerging credit or deposit account needs for consideration.

Evaluating feedback from potential customers whose needs reveal gaps in a bank’s product offerings, features, or credit standards can help document a business case for developing new products or terms, or revisiting credit standards, to level the playing field and increase the bank’s competitive market position.

Expanding customer relationships and wallet share

Finally, banks should consider deepening relationships arising from the institution’s CRA and fair lending efforts. Consider whether organizations receiving community development services or investments have credit or deposit needs that the bank can meet. Can the bank leverage its community outreach efforts and partnerships to build trust and improve reputation, not just in LMI neighborhoods, but across all segments of the communities it serves? Can information the bank gathered through community partnerships and outreach efforts reduce customer acquisition costs?

For consumer and small business customers, there may be ways to increase wallet share profitably. For example, do small businesses, for whom the bank has provided technical assistance, need and qualify for additional deposit or credit relationships? Do consumers completing financial education have needs the bank can meet?

Does the bank offer secured cards or lend through fintech partnerships? If so, those customers may be good candidates for more traditional banking products and services such as unsecured cards, auto loans, mortgages, deposit products, etc. In other words, this approach supports relationship deepening and long-term product migration.

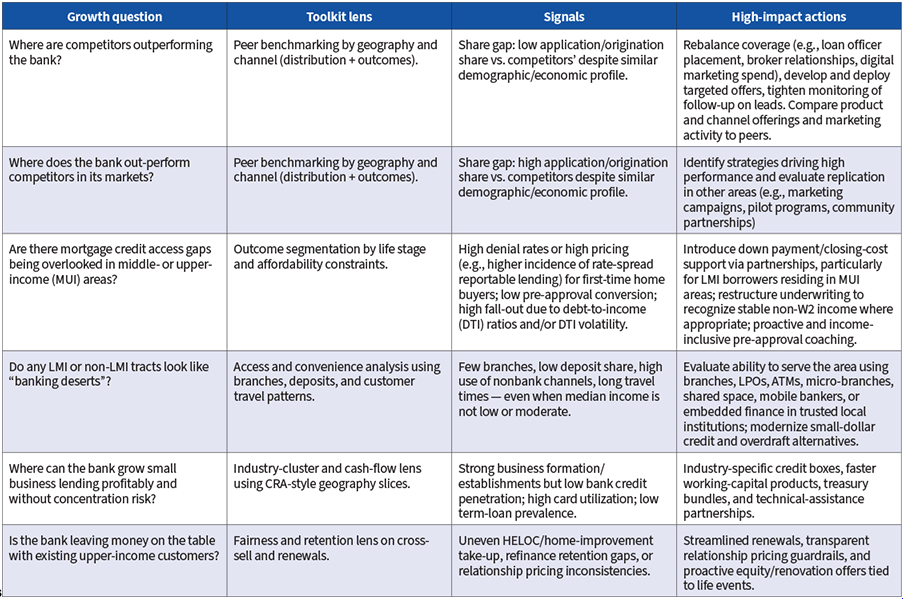

FIGURE 2. From growth questions to high-impact actions

Figure 2 provides a snapshot of growth questions your CRA and fair lending compliance program tools can help leverage into high-impact actions.

Conclusion

In addition to supporting CRA and fair lending risks, a bank’s compliance team can be a critical part of its growth strategy. Banks can use CRA and fair lending capabilities as a strategic advantage by treating them as a market-intelligence and product-design toolkit for the enterprise — not just a compliance function. When a bank combines routine fair lending and CRA analyses with market data, profitable gaps can surface that scale with consistent decisioning and pricing.

Endnotes

Map courtesy of RiskExec, Inc. (n.d.). RiskExec HMDA module. Accessed February 16, 2026.

Community Reinvestment Act; Interagency Questions and Answers Regarding Community Reinvestment; Notice, 75 Fed. Reg. 11642 (Mar. 11, 2010).

Fed. Fin. Insts. Examination Council, Interagency Fair Lending Examination Procedures, at 7, 21 (Aug. 2009), https://www.ffiec.gov/sites/default/files/media/press-releases/2021/2021-june-17-fairlend.pdf [hereafter, Interagency Fair Lending Examination Procedures]; see also id. at 2 (determine whether an institution offers any loan "program that is specifically designed to assist certain underserved populations").

Community Reinvestment Act; Interagency Questions and Answers Regarding Community Reinvestment; Guidance, 81 Fed. Reg. 48506, 48517 (July 25, 2016) [hereafter, CRA Q&A].

CRA Q&A at 48519

Check out the ABA May/June 2025 Issue HERE

About the Authors

LYNN WOOSLEY, CRCM, is a Managing Director with Asurity Advisors and a member of the Editorial Advisory Board for ABA Risk and Compliance magazine. Lynn has over 30 years of experience in risk management, spanning both financial services and regulatory environments. She is an expert in consumer protection, including fair lending, fair servicing, community reinvestment, and UDAAP. Before joining Asurity Advisors, Lynn led the fair banking practice for an advisory firm. She has also held multiple leadership positions, including Senior Vice President and Fair and Responsible Banking Officer, within the Enterprise Risk Management division of a top 10 bank. Prior to joining the private sector, Lynn served as Senior Examiner and Fair Lending Advisory Economist at the Federal Reserve Bank of Atlanta. Reach her at lwoosley@asurity.com.

OLIVIA KELMAN focuses her practice on representing clients in litigation, compliance, and enforcement matters, with a concentration on fair housing and fair and responsible lending and servicing. She regularly advises clients seeking to identify and mitigate fair housing and fair lending risk, or in defending fair lending claims, in areas relevant to the client’s business, including redlining, branching, pricing, underwriting, marketing, steering, servicing, modeling, and reasonable accommodations.

SIGN UP FOR UPDATES

Never miss our news, insights or events.

FEATURED NEWS